This booklet is the solution to many international families’ needs as they - and the institutions that serve them - grasp the significance of FATCA and the impact it is likely to impose on their existing trusts and succession plans.

Winterbotham is headquartered in The Bahamas and is dedicated to providing tailor-made financial and fiduciary services to entrepreneurs, their families and advisors worldwide. Winterbotham works closely with financial institutions and other service providers to develop and implement the very best tried and tested solutions for its clients. Winterbotham is a fully licensed and regulated bank and trust company in The Bahamas and is a specialist provider of bespoke trustee services and the demanding administrative support such services demand.

IPG is an estate, inheritance planning and family office consultancy, assisting professional intermediaries in the structuring of their clients’ affairs. IPG’s services are bespoke, client-driven and confidential – essential ingredients demanded by today’s wealthy families who hold many highly diversified assets and interests. IPG determines how to optimise the structuring of each family’s cross-border holdings thereby ensuring their proper management, both for the present and for the long term.

2GUSB is a prime example of Winterbotham and IPG’s innovative approach - firstly to identifying the problem and then providing the solution in an intelligible and coherent manner – and all housed in one user-friendly booklet. The solution is supported by legal advice from eminent Bahamian and United States counsel.

Winterbotham is located in The Bahamas, Uruguay and Hong Kong and IPG has offices in The Bahamas and Switzerland.

Winterbotham offers a comprehensive range of trust administrative services to its clients, be they individuals, families or corporations. With over $2 billion in trust assets under administration, Winterbotham has a wealth of experience in advising on and establishing a wide variety of trusts, each one tailored to address a number of specific needs. Winterbotham provides full trusteeship and professional trust administration services to all its relationships and devotes the care and attention that each one demands. The objectives of Winterbotham’s trust and company structures vary greatly, but include:

Trust Objectives

|

Company Objectives

|

Winterbotham in The Bahamas acts as trustee of the 2GUSB trusts and is responsible for all daily management and administrative needs.

IPG is an estate, inheritance planning and family office consultancy, assisting professional intermediaries in the structuring of their clients’ affairs. IPG’s services are bespoke, client-driven and confidential – essential ingredients demanded by today’s wealthy families who hold many highly diversified assets and interests. IPG determines how to optimise the structuring of each family’s cross-border holdings, thereby ensuring their proper management, both for the present and for the long term. IPG structures its solutions to suit very specific needs. IPG’s core services include:

|

|

The Foreign Account Tax Compliance Act (FATCA) was enacted in March 2010 by US Congress and its impact on many current international trust structures is going to be important. The central theme of the new Act is to ensure that US tax payers throughout the world are held accountable for US tax no matter where they reside or where the income is earned. In order to achieve this objective, the law has introduced the concept of a “Foreign Financial Institution” (FFI), which is a bank, broker or similar institution situated abroad. To avoid withholding on funds received for its own or client accounts, each FFI will have to register with the US Internal Revenue Service (IRS) and comply with stringent reporting and withholding requirements.

So how does this affect trusts? By nature of their business, nearly all professional trust companies performing trustee services (wherever in the world they are situated) will be designated as FFIs. One of the first things they must do is to ascertain which of the many trusts they administer are also FFIs in their own right too.

According to US tax principles, a trust is either a domestic or foreign Trust or a Grantor or Non-Grantor Trust. Income earned by a US Grantor trust will be reported on the grantor’s tax return and will not be affected by FATCA. However, a foreign Non-Grantor Trust will be affected.

Foreign Non-Grantor Trusts holding bankable assets and investments could be designated FFIs in their own right and will either have to enter into an agreement with the IRS or incur a 30% withholding penalty - not only on US sourced income, dividends and other similar income, but also on the gross proceeds of the sale of the associated assets, stocks etc. The agreement will cover the filing of information on US tax paying beneficiaries and will also extend to submitting details of non-US beneficiaries of the non-grantor trust.

Trusts / beneficiaries that choose not to disclose all the relevant information to the IRS will not have their personal details disclosed and initially they will have the 30% withholding regime imposed on them. Eventually, however, they will be required to close their account(s) with the FFI.

For many families the prospect of the 30% withholding on US income and asset sales will be too much to bear and in any case it is only a short term option. On the other hand, disclosing information and filing reports to the IRS on their trusts’ affairs and their interested parties will be unpalatable too and in the eyes of many unreasonable. Such families, and their trustees, will be keen to find some sort of compromise – or indeed a solution.

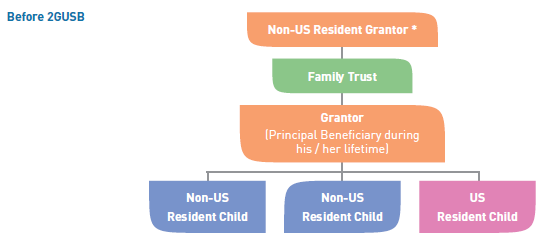

Many of today’s international trust structures have beneficiaries with a wide variety of domiciles with differing tax and reporting obligations. The arrival of FATCA has implications for many of these structures and it is especially important to ascertain whether any second generation beneficiaries have US tax exposure or reporting obligations. Should any such person be identified within a structure, remedial measures are recommended.

A typical trust structure today may look something similar to this:

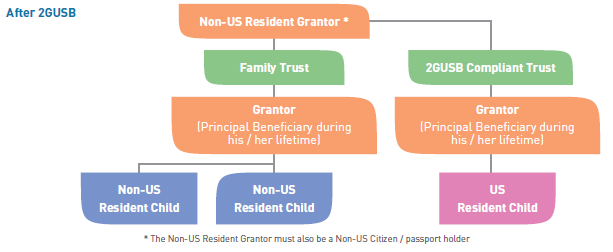

Under FATCA the above structure will qualify as a “Foreign Financial Institution” (FFI) and depending on where it is managed is likely to be obliged to enter into an agreement with the IRS or incur a 30% withholding penalty. The 2GUSB solution provides for a new standalone tax compliant trust structure for the ultimate benefit of the US child(ren) and remoter issue of non-US tax resident Grantors. 2GUSB is a Grantor trust established in The Bahamas specifically for the Grantor’s children born or living in the US. This enables the Grantor to focus the family’s US estate and inheritance planning needs within an internationally recognized and US compliant solution.

If deemed desirable in the future, the 2GUSB Grantor trust can be redomiciled from The Bahamas to a favourable US State, in accordance with the laws prevailing at that time.

Trust Structure

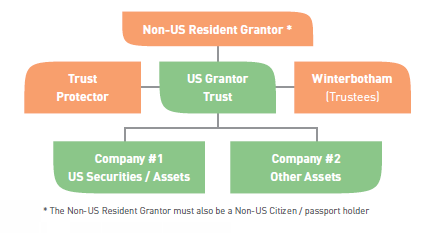

The 2GUSB solution comprises a US Grantor trust established under Bahamas trust law by a non-US Resident Grantor. As trustees of the trust, Winterbotham are responsible for managing and maintaining the trust and for ensuring the entire structure is administered correctly. The trust’s assets are held by one of two Bahamas registered companies depending on the nature of those assets. All US securities and other US situated assets are held by Company #1 and all other assets are held by Company #2.

The 2GUSB solution also includes a Protector who is chosen by the Grantor and whose powers are defined in the trust deed. The powers include removing and appointing new trustees; changing the governing law of the trust and its place of administration; acting in the event of the Grantor’s incapacity and varying the terms of the trust.

Glossary of 2GUSB Terms

| Grantor | Person who creates a trust by completing and signing a written trust deed and who transfers assets into the trust. |

| Trustees | Company responsible for the administration and maintenance of the trust structure. |

| Protector | Person chosen by the Grantor and whose powers are defined in the trust deed. |

| Trust Deed | Document signed by the Grantor and the Trustees governing how the trust will be administered and on whom certain powers are bestowed. |

| Beneficiaries | Persons, usually family members, who are expected to benefit under the terms of the trust. |

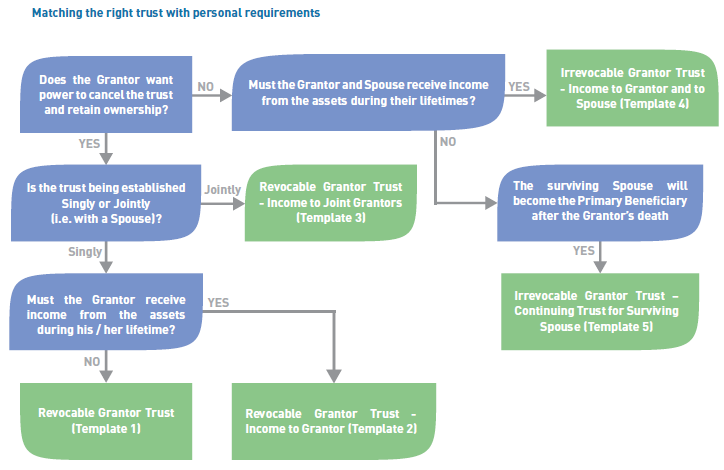

2GUSB provides five trust templates to suit different preferences and circumstances. The five are:

As a guide to finding the most suitable solution for each case, we have devised a number of questions for navigating to one of the options mentioned above.

“Revocable Grantor Trust”: A trust whereby provisions can be altered or cancelled with powers given to the Grantor(s) and the assets are then paid back to the Grantor(s). During the life of the trust, income earned can be paid to the Grantor(s) and after his / their passing the assets transfer to the Grantor’s children.

“Irrevocable Grantor Trust”: A trust which cannot be modified or cancelled by the Grantor(s). The Grantor, having transferred assets into the trust, ceases to have rights of ownership to the assets. The Grantor is the principal trust beneficiary, to whom assets can be paid during his / her lifetime. Income earned can continue to be paid to the Grantor(s) until their passing, whereupon the assets pass to the children.

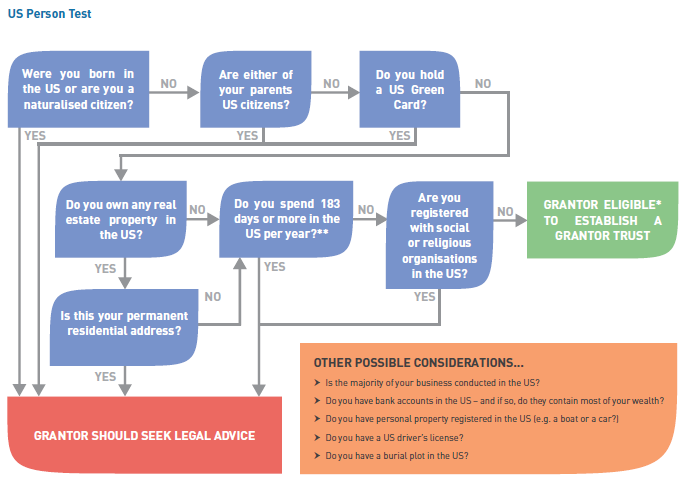

As we have seen in “FATCA and The Implications”,the central theme of the new Act is to ensure that US tax payers throughout the world are held accountable for US tax no matter where they reside or where the income is earned. Whilst the focus of this (within the context of 2GUSB) is primarily on the second generation beneficiary, it is also important to test the credentials of trust settlors or grantors to ensure they are eligible to establish a US Grantor trust. To establish a US Grantor trust compliant with current US tax law, it is essential that the Grantor is a non-US person.

If the current status of the Grantor within a trust structure is unknown, we have devised a test to determine which persons are likely to be classified as being US persons / tax payers under the US tax principles and which may not. The test is by no means exhaustive and should be treated with a certain degree of caution, but it does contain many of the criteria by which individuals are commonly caught by the provisions of US tax law.

* Eligibility can only be fully confirmed upon completion of the 2GUSB Trust

Acceptance Form.

** Substantial U.S. Presence Test. Under the general rule

for U.S. tax residency, foreign nationals are “substantially present,”

in the United States if they are present for at least 31 days in the current calendar

year, and their U.S. days over 3 calendar year equal or exceed 183 days based on

a formula. The 183-day formula considers all of the U.S. days in the current calendar

year, plus 1/3 of the U.S. days in the prior year, plus 1/6 of the days in the year

before the prior year. Foreign nationals whose presence in the United States satisfies

the substantial formula are resident aliens and taxed like U.S. citizens.

We emphasise that our US Person Test is indicative only and for a definitive verdict an opinion from US tax counsel would need to be obtained.

The questions posed within the US Person Test can also be addressed to a second generation trust beneficiary to indicate their own US tax status (with the same caveats emphasised above still applying).

Bahamas trust law draws on its historical links with England and English common law and its equitable principles. However, with the introduction of a number new statutes passed by its parliament, Bahamas trust law has evolved in a number of very interesting ways – so much so that today it has become one of the most attractive trust jurisdictions in the world.

The principal trust and trustee related laws enacted in The Bahamas are:

|

|

Some of the key features that are available to trusts and settlors created under the law of the Bahamas include: